Retirement calculator: Estimate your retirement savings and monthly retirement income

Planning retirement is not just about reaching a large number in an account. Most people want a simpler answer: Will I have enough each month to live comfortably? That’s why this retirement calculator is built as both a retirement savings calculator and a monthly retirement income calculator.

Instead of only estimating a future balance, this tool helps you plan your retirement paycheck by combining:

Your projected retirement savings at retirement age

A withdrawal strategy (such as the 4% rule)

Monthly Social Security estimates

Pension income (if applicable)

Part-time or flexible income (optional)

Healthcare costs (a major retirement expense)

Inflation adjustment (to preserve purchasing power)

A simple household paycheck plan to keep spending clear

This structure is especially helpful for retirees and older adults who want a plan that is easy to understand without complicated spreadsheets.

How to use this retirement calculator?

To get a meaningful result, start with the core inputs:

Current age and retirement age

Current retirement savings (401(k), IRA, brokerage, etc.)

Monthly contribution you add today

Expected annual return (use conservative scenarios too)

Inflation (optional, but recommended)

Monthly spending goal in retirement

Social Security and pension income estimates

Healthcare costs (often underestimated)

Withdrawal strategy (4% rule or a custom rate)

When you click Calculate, the tool provides:

Projected balance at retirement

Estimated monthly retirement paycheck from savings

Total monthly income including Social Security/pension

Monthly gap (surplus or shortage vs your expense assumptions)

An estimate of the monthly contribution needed to close the gap

This makes the calculator useful not only for investing, but also for real-world household planning.

How retirement rrowth is estimated?

This retirement savings calculator models growth over time based on:

Starting balance

Ongoing monthly contributions

Compounding returns

Years until retirement

Your projected retirement balance is an estimate, not a guarantee. Markets fluctuate and returns vary. That’s why it’s smart to run at least three scenarios:

Conservative: 4-5%

Moderate: 6-7%

Aggressive: 8-9%

Most retirement plans improve when you focus on the controllable variables:

Contribute consistently

Reduce fees when possible

Avoid panic selling

Increase contributions gradually over time

The retirement paycheck concept (What most people actually need)

A retirement paycheck is the monthly income you can reasonably expect to have when you stop working. It typically comes from:

Social Security

Pension income (if you have one)

Withdrawals from retirement savings

Optional income (part-time work, rental income, etc.)

This calculator estimates your monthly paycheck from savings using your selected withdrawal strategy (for example, the 4% rule). Then it adds Social Security and other income to estimate total monthly resources.

From there, it compares your income to:

Monthly spending goal

Monthly healthcare estimate

The result is the most important number on the page:

Your monthly gap: whether you are likely to have enough.

Inflation: Why enough money changes over time?

Inflation reduces purchasing power. Even if your retirement account grows, prices usually rise too.

If you select Show spending in today’s dollars, the calculator inflates your spending goal forward to retirement age so you can compare apples to apples.

This is a premium planning feature because it forces realistic assumptions. A comfortable $4,500/month today may require significantly more in retirement-year dollars.

Withdrawal strategy: The 4% rule and why people adjust it?

The 4% rule is a simple guideline: withdraw roughly 4% of your retirement portfolio per year. It’s popular because it’s easy to understand.

However, many retirees choose more conservative withdrawal rates (3.5% or similar) for:

Longer life expectancy

Higher market uncertainty

Desire to leave an inheritance

Higher healthcare expenses

This calculator supports multiple strategies plus a custom option so your plan can match your comfort level.

Introducing household paycheck planner: A simple tool retirees actually use

Many people can’t stick to a plan because budgets feel confusing. The Household Paycheck Planner helps simplify that.

It breaks your estimated monthly income into three buckets:

Essentials (housing, food, utilities, bills)

Lifestyle (travel, dining, hobbies, entertainment)

Giving/Goals (family support, charity, personal goals)

This feature is transferable beyond finance because it is essentially a simple household planning tool that any family can use ; even before retirement.

Use our Compound Interest Calculator and Debt Payoff Calculator to see how savings growth and debt elimination work together.

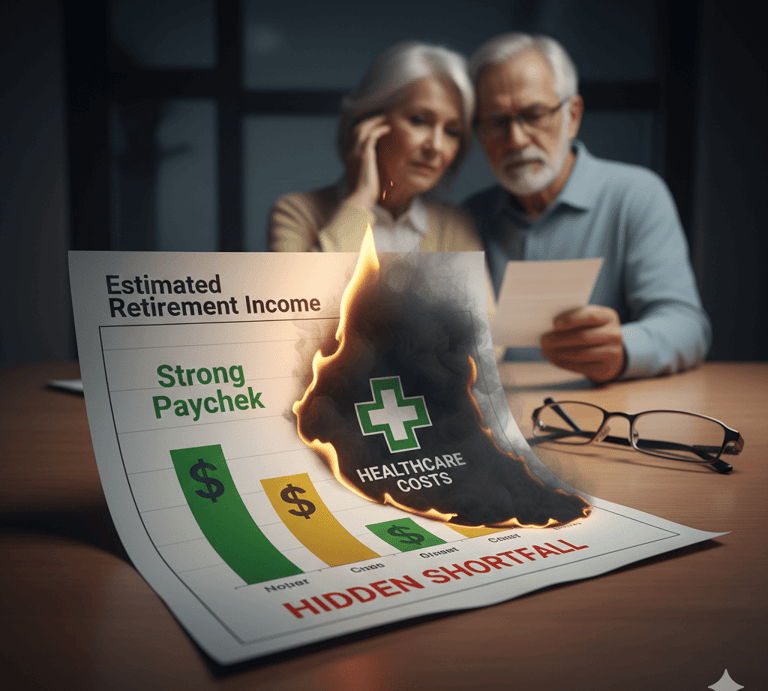

Healthcare costs in retirement: The overlooked expense that breaks most budgets

For many retirees, healthcare costs become the biggest surprise expense ; because they don’t show up clearly until after you stop working. Even with Medicare, most households still pay meaningful out-of-pocket costs every month. That’s why this retirement calculator includes a dedicated monthly healthcare cost line item: it helps you estimate a more realistic retirement budget, not just a retirement balance.

When people search online for retirement planning help, they often use everyday phrases like:

“How much does healthcare cost in retirement?”

“Average monthly medical expenses for retirees”

“Medicare costs per month”

“How much should I budget for medical expenses in retirement”

“Does Medicare cover dental and vision”

“Retirement healthcare costs calculator”

“Out-of-pocket costs with Medicare”

“Long-term care costs”

What healthcare expenses usually include?

Even if Medicare covers a portion, retirees commonly still pay for:

1) Medicare premiums (monthly)

Many retirees pay monthly premiums for Medicare coverage (especially when choosing additional coverage beyond basic Medicare). This often becomes a fixed monthly bill ; similar to a utility payment ; so it should be accounted for in your retirement paycheck plan.

2) Prescription drugs and medications

Medication costs can fluctuate throughout the year. Some people pay small copays; others face higher costs depending on prescriptions, pharmacy coverage, or specialty medications. This is one reason average healthcare budgets can be misleading ; your costs may rise as needs change.

3) Copays, deductibles, and specialist visits

Even with coverage, you may still pay:

doctor visit copays

lab work costs

imaging (X-rays, MRIs)

specialist appointments

deductibles before coverage kicks in

These add up quickly, especially if you manage chronic conditions.

4) Dental and vision costs

A common retirement shock is realizing that dental and vision are often not fully covered in the same way people expect. Routine cleanings, fillings, crowns, dentures, eyeglasses, and contacts can become a meaningful annual expense ; so it’s helpful to convert that into a monthly budget estimate.

5) Long-term care planning

Long-term care is one of the most searched and most underestimated retirement costs. Even if you never need full-time care, you may face costs for:

in-home assistance

mobility support

rehabilitation services

assisted living

nursing care

You don’t need to predict the exact outcome, but adding a realistic healthcare line item helps create a more resilient plan.

Why adding healthcare makes your retirement plan more accurate?

Most retirement calculators only estimate savings growth. But retirees don’t live on account balances, they live on monthly cash flow. If your retirement paycheck looks strong on paper but doesn’t include healthcare, you can end up with a hidden shortfall.

Including healthcare helps you:

estimate a more realistic monthly retirement income target

avoid underestimating your spending needs

stress-test your plan against rising costs

reduce the chance of running out of money later in retirement

Practical tip: If you’re unsure what to enter, start with a conservative monthly estimate, then run a second scenario with a higher number. This gives you a range instead of a single perfect guess.

Retirement Healthcare Costs FAQ

1) How much should I budget for healthcare costs in retirement?

A practical starting point is to budget a monthly healthcare amount that covers Medicare premiums, prescriptions, and routine visits. Many retirees underestimate these expenses because costs are spread across premiums, copays, and medication refills. If you’re unsure, run two scenarios in the calculator: a conservative estimate and a higher estimate to see how sensitive your retirement plan is to medical costs.

2) What are average monthly medical expenses for retirees?

Average monthly medical expenses for retirees vary widely depending on location, health needs, and coverage choices. Some households spend a relatively steady amount, while others see costs rise due to chronic conditions, specialist care, or high-cost prescriptions. That’s why a retirement healthcare costs calculator is useful ; your real number depends on your situation, not a generic average.

3) Does Medicare cover dental and vision?

Many retirees ask this because dental and vision costs can become significant. Dental care (cleanings, fillings, crowns, dentures) and vision care (eye exams, glasses, contacts) may not be fully covered in the way people expect. Planning for these costs as part of your monthly retirement budget can prevent surprise expenses later.

4) How do I estimate Medicare costs per month?

To estimate Medicare costs per month, include:

monthly premiums (depending on your plan choices)

prescription drug costs

copays and deductibles

routine doctor visits and specialist visits

A simple way is to review your current annual medical spending and convert it into a monthly estimate, then adjust upward if you expect increased usage with age.

5) What about long-term care costs in retirement?

Long-term care is one of the most searched retirement concerns because it can be expensive and unpredictable. Even if you never need full-time assisted living, many people face costs for in-home help, rehabilitation, mobility support, or assisted living at some point. Adding a monthly healthcare estimate helps your plan stay realistic and protects your retirement paycheck from hidden risk.

Quick Summary: Retirement Healthcare Planning

Understanding retirement healthcare costs, Medicare premiums per month, average medical expenses in retirement, and long-term care costs is essential for building a realistic retirement income plan. A retirement healthcare budget calculator helps estimate monthly medical expenses, project out-of-pocket costs, and adjust your retirement savings strategy to avoid income shortfalls later in life.

6) How much do I need to retire?

It depends on your monthly spending needs, retirement age, expected Social Security, and withdrawal strategy. This calculator estimates both your retirement balance and your monthly income to show whether you are on track.

7) Is this a 401(k) retirement calculator?

Yes. You can use it for 401(k), IRA, Roth IRA, brokerage savings, or a combination, as long as you enter a total starting balance and contributions.

8) What return should I assume?

Many planners test 5–7% long-term. Use multiple scenarios. Higher assumptions can look great on paper but may reduce reliability.

9) Does this include taxes?

This tool includes an optional effective tax rate estimate to show a more realistic net monthly income. Taxes vary widely, so treat this as a planning estimate only.

10) What if my gap is negative?

A negative gap means projected income is below expenses. You can close it by increasing contributions, delaying retirement, lowering spending goals, increasing income, or using a more conservative inflation assumption.

11) Should I count Social Security?

Yes, but use conservative numbers. If unsure, run with and without Social Security to see how sensitive your plan is.

Final Thoughts

A strong retirement plan is not about perfection. It’s about clarity and flexibility. This retirement calculator helps you see:

What you may have at retirement

What your monthly income could look like

Whether that income supports your lifestyle

What changes could improve your outcome

Use this retirement calculator to test scenarios and make small improvements. Over time, consistent actions compound into meaningful retirement security.

Use our Compound Interest Calculator and Debt Payoff Calculator to see how savings growth and debt elimination work together.

Independent financial planning tools for educational purposes only. Not affiliated with Google, AdSense, or financial institutions.

© 2026 Unlock Your Wealth and Success™. All Rights Reserved.

Terms of Service