How to use this free loan payment calculator to estimate monthly payments?

Our loan payment calculator helps you quickly determine your estimated monthly payment, total interest paid, and total repayment amount based on three essential inputs: loan amount, interest rate, and loan term.

Whether you're planning to take out a personal loan, auto loan, student loan, or small business loan, understanding your monthly financial obligation before signing an agreement is critical. This monthly loan payment calculator allows you to compare different borrowing scenarios and make smarter financial decisions.

To use the calculator:

Enter your total loan amount.

Input the annual interest rate offered by your lender.

Specify the loan term in years.

Click Calculate Payment.

The tool will instantly display:

Your estimated monthly payment

Total amount repaid over the life of the loan

Total interest paid

This gives you a clear financial picture before committing to a loan agreement.

How loan payments are calculated (amortization explained)?

Most installment loans use a formula known as the loan amortization formula. Amortization spreads repayment over fixed monthly payments across a set period of time.

Each payment consists of:

A portion applied toward the loan principal

A portion applied toward interest

In the early stages of a loan, a larger percentage of each payment goes toward interest. As the principal balance decreases, more of each payment goes toward reducing the principal.

The standard formula used in this loan interest calculator is:

Monthly Payment = P × r × (1 + r)^n ÷ ((1 + r)^n − 1)

Where:

P = Loan principal (amount borrowed)

r = Monthly interest rate (annual rate divided by 12)

n = Total number of payments

This formula ensures your loan is fully paid off at the end of the term, assuming fixed interest and consistent monthly payments.

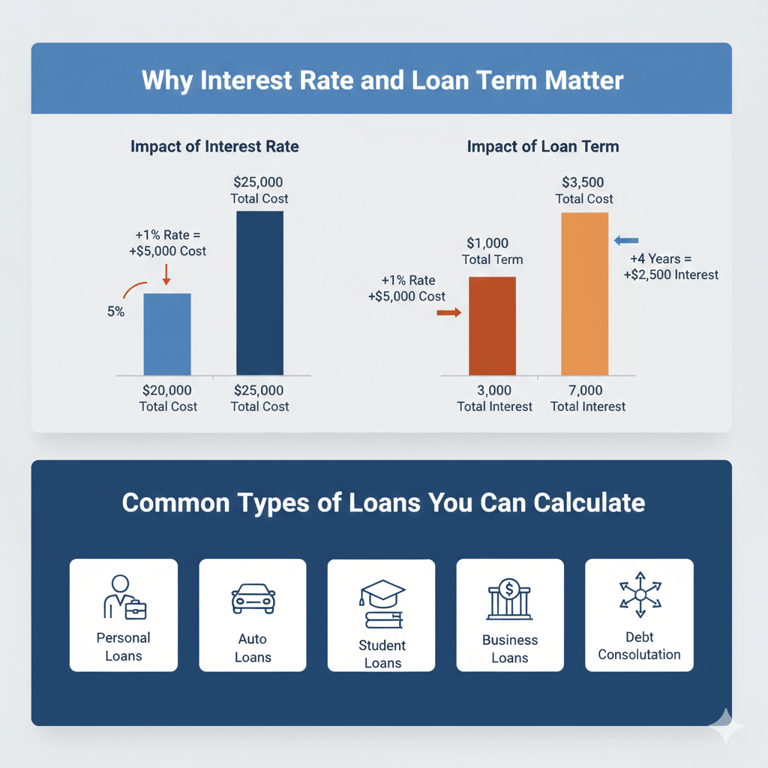

Why interest rate and loan term matter?

Two of the most important variables in any loan are the interest rate and the repayment period.

Interest rate

A small difference in interest rate can significantly affect the total cost of borrowing. For example:

A $20,000 loan at 5% for 5 years costs substantially less than the same loan at 8%.

Even a 1% increase can add hundreds or thousands of dollars over time.

Using a loan interest calculator helps you see exactly how rate changes impact your monthly obligation.

Loan term

Loan term refers to the length of time you have to repay the loan.

A shorter loan term increases your monthly payment but reduces total interest paid.

A longer loan term lowers your monthly payment but increases total borrowing costs.

For example:

A 3-year loan may have higher monthly payments but significantly less total interest compared to a 7-year loan for the same amount.

This calculator allows you to compare different loan durations instantly.

Common types of loans you can calculate

This loan payment calculator works for most fixed-rate installment loans, including:

Personal loans

Auto loans

Student loans

Business loans

Debt consolidation loans

Home improvement loans

If the loan has a fixed interest rate and a defined term, this calculator can estimate payments accurately.

For mortgages specifically, you may want to use a dedicated mortgage affordability calculator to account for property taxes and insurance.

Benefits of using a loan payment calculator before borrowing

Before signing any lending agreement, running your numbers through a loan payment calculator can help you:

1. Compare lenders

Different lenders may offer varying interest rates. This tool helps you understand how rate differences affect your finances.

2. Plan your budget

Knowing your estimated monthly payment allows you to determine whether the loan fits within your monthly income and expenses.

3. Avoid overborrowing

Many borrowers focus only on approval amounts. Instead, calculate what you can realistically afford to repay.

4. Reduce financial stress

Understanding repayment obligations in advance reduces the risk of default and financial strain.

How extra payments impact your loan?

Many borrowers don’t realize that making additional principal payments can significantly reduce total interest paid.

If you:

Make extra monthly payments

Add occasional lump-sum payments

Round up payments each month

You shorten the loan term and reduce overall borrowing costs.

While this calculator estimates standard payments, you can experiment by reducing the loan term to simulate accelerated repayment strategies.

Factors that can affect actual loan payments

While this calculator provides accurate estimates based on mathematical formulas, actual loan payments may vary depending on:

Origination fees

Prepayment penalties

Variable interest rates

Insurance requirements

Late fees

Always review your lender’s official amortization schedule before signing a loan agreement.

Frequently Asked Questions

What is a good interest rate for a personal loan?

A good interest rate depends on your credit score, income stability, and market conditions. Borrowers with excellent credit typically qualify for lower interest rates.

Does paying off a loan early save money?

Yes. Paying off a loan early reduces total interest paid, especially if there are no prepayment penalties.

Can I use this calculator for variable-rate loans?

This tool is designed for fixed-rate loans. Variable-rate loans may change over time and require more advanced projections.

How do I lower my monthly payment?

You can lower monthly payments by:

Increasing the loan term

Negotiating a lower interest rate

Reducing the loan amount

However, extending the term increases total interest paid.

Final Thoughts

Making informed financial decisions starts with understanding your repayment obligations. This loan payment calculator gives you clarity before you borrow, helping you compare options and avoid costly mistakes.

Use this tool whenever you:

Apply for a new loan

Compare refinancing offers

Evaluate debt consolidation

Plan large purchases

Smart borrowing begins with smart calculations.

Use our Mortgage Affordability Calculator and Debt Payoff Calculator to evaluate your borrowing power and build a smarter repayment strategy.

Independent financial planning tools for educational purposes only. Not affiliated with Google, AdSense, or financial institutions.

© 2026 Unlock Your Wealth and Success™. All Rights Reserved.

Terms of Service