Debt payoff calculator page

This version includes:

Strong keyword coverage

Snowball vs Avalanche targeting

Debt consolidation angle

Side hustle & lump sum angle

Long-tail FAQ capture

Authority tone

Evergreen structure

Replace your current written section with this.

Debt payoff calculator (Snowball vs Avalanche + Extra Payment Strategy)

Paying off debt is one of the most powerful financial decisions you can make. Whether you are managing credit card balances, personal loans, student loans, or other high-interest obligations, understanding your payoff timeline can dramatically improve financial clarity and reduce long-term interest costs.

This Debt Payoff Calculator helps you estimate how long it will take to become debt-free based on your balance, interest rate, minimum payment, and additional contributions. You can also test real-world scenarios such as adding side income, applying tax refunds, using annual bonuses, or comparing a debt consolidation loan.

The goal is not just repayment ; it is strategic acceleration.

How this debt payoff calculator works?

This calculator simulates your debt balance month-by-month.

Each month:

Interest accrues based on your annual percentage rate (APR).

Your payment is applied (minimum + extra + side income).

Optional lump sums or bonuses are applied in selected months.

The process repeats until your balance reaches zero.

The tool calculates:

Total payoff time (months and years)

Total interest paid

Total amount repaid

The financial impact of additional income

The potential difference with consolidation

This gives you a realistic estimate of how your debt declines over time.

Use our Loan Payment Calculator and Compound Interest Calculator to compare borrowing costs and understand how interest works over time.

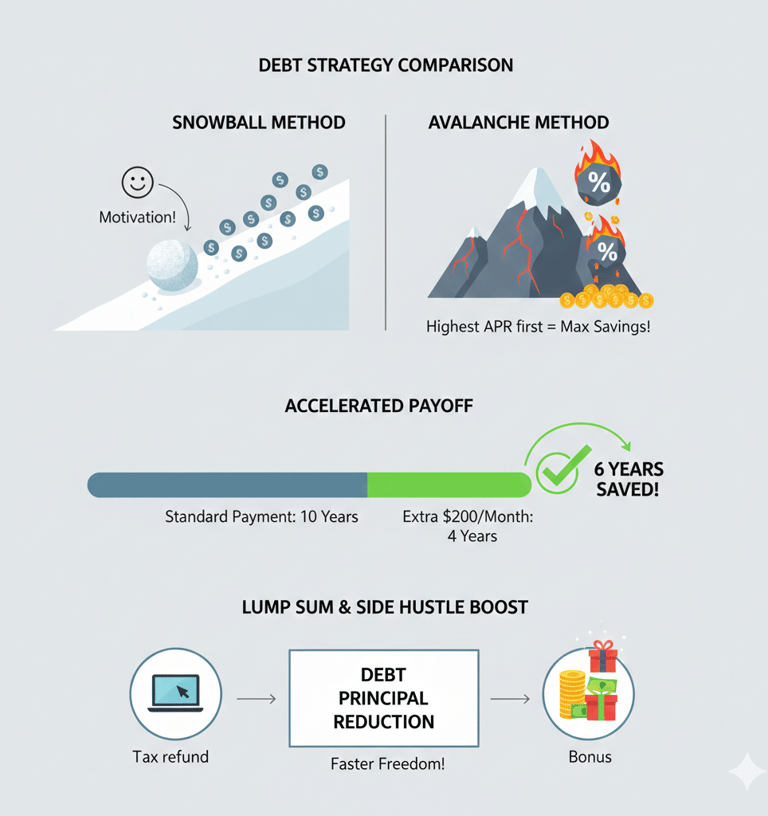

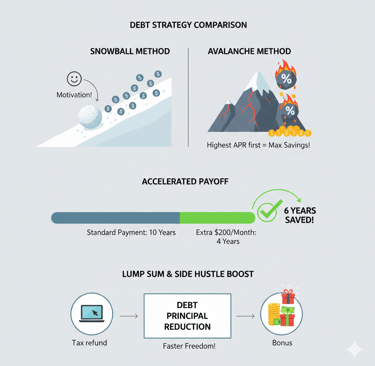

Snowball vs Avalanche method explained

Although this calculator uses total balance and average APR, it supports both major debt payoff strategies conceptually.

Debt snowball method

The Snowball method focuses on paying off the smallest debts first while making minimum payments on larger ones.

Benefits:

Quick psychological wins

Momentum building

Higher motivation

Simplified focus

Many people stick to repayment plans longer using the snowball method because it provides visible progress early.

Debt avalanche method

The Avalanche method focuses on paying off the highest interest rate debts first.

Benefits:

Minimizes total interest paid

Mathematically optimal

Reduces long-term borrowing cost

While avalanche usually saves more money, snowball may improve consistency. The best strategy is the one you can sustain.

The power of extra monthly payments

Small consistent payments can create dramatic long-term savings.

For example:

A $25,000 balance at 18% APR with only minimum payments could take many years to eliminate and generate thousands in interest.

Adding just $200 extra per month may:

Cut payoff time by years

Save thousands in interest

Reduce financial stress faster

Consistency matters more than occasional large payments.

Using side hustle income to accelerate debt freedom

One of the most powerful features of this calculator is the ability to simulate additional monthly income.

You can test:

Freelance earnings

Gig economy work

Online business revenue

Overtime pay

Commission income

Even an additional $150–$300 per month can significantly shorten your payoff timeline.

The psychological impact of watching months disappear from your repayment schedule can reinforce positive financial habits.

Use our Loan Payment Calculator and Compound Interest Calculator to compare borrowing costs and understand how interest works over time.

Applying tax refunds and lump sum payments

Tax refunds, bonuses, or one-time cash inflows are powerful tools when directed toward high-interest debt.

Instead of spending a $2,000 tax refund, applying it toward principal reduces future interest accumulation immediately.

This calculator allows you to simulate:

When the lump sum is applied

How much time it saves

How much interest it eliminates

Lump sums reduce the compounding effect of high-interest debt.

Annual bonus strategy

If you receive an annual bonus or seasonal income spike, directing even a portion of it toward debt repayment can create exponential impact.

Because interest compounds monthly, applying a bonus at the right time reduces future interest accumulation across the remaining balance.

This tool allows you to model recurring yearly contributions and measure their cumulative effect.

Debt consolidation comparison

Debt consolidation is often marketed as a solution for high-interest debt.

With consolidation, you:

Replace multiple debts with one loan

Potentially reduce your interest rate

Simplify payments

Extend or shorten repayment term

However, consolidation is not always cheaper.

If you extend the term significantly, you may lower monthly payments but increase total interest.

This calculator allows you to:

Compare your current payoff strategy

Test a lower consolidation APR

Evaluate origination fees

Apply extra payments to the consolidation loan

This gives you a side-by-side view of total interest and payoff duration.

When consolidation makes sense?

Debt consolidation may be beneficial when:

The new APR is significantly lower

You avoid extending the repayment term too long

You remain disciplined with spending

You continue making extra payments

Consolidation is a tool ; not a solution by itself.

Common mistakes in debt repayment

Paying only minimums

Ignoring high APR accounts

Consolidating without comparing total cost

Using lump sums for consumption instead of reduction

Stopping extra payments after partial progress

This calculator helps you visualize the long-term cost of these decisions.

Use our Loan Payment Calculator and Compound Interest Calculator to compare borrowing costs and understand how interest works over time.

Frequently Asked Questions

How long will it take to pay off my debt?

It depends on your balance, APR, and monthly payment. Increasing your payment consistently shortens the payoff period dramatically.

Is debt snowball or debt avalanche better?

Avalanche usually saves more money in interest. Snowball may improve consistency due to psychological momentum.

Does debt consolidation lower interest?

Sometimes. It depends on the new interest rate, term length, and fees. Always compare total repayment cost, not just monthly payment.

How much interest will I pay over time?

This calculator estimates total lifetime interest based on your inputs and payment strategy.

Can side income really make a difference?

Yes. Even modest additional monthly contributions reduce principal faster, lowering interest compounding.

Should I use tax refunds to pay off debt?

If your debt carries high interest (e.g., credit cards), applying lump sums toward principal often produces significant long-term savings.

What is a good interest rate for consolidation?

It varies by credit score and lender, but ideally the consolidation APR should be meaningfully lower than your current weighted average rate.

Why this debt payoff calculator is different?

Unlike simple calculators, this tool:

Allows side income simulation

Supports lump sum timing

Models annual bonuses

Compares consolidation scenarios

Encourages strategic planning

Emphasizes behavioral sustainability

It is not just a payoff estimator ; it is a debt strategy planner.

Final Thoughts

Debt freedom is not achieved through math alone. It requires clarity, discipline, and strategy.

By understanding how interest compounds, how extra income accelerates repayment, and how consolidation impacts total cost, you gain control over your financial timeline.

Use this Debt Payoff Calculator to test scenarios before making decisions. Small changes today can save years and thousands of dollars tomorrow.

Independent financial planning tools for educational purposes only. Not affiliated with Google, AdSense, or financial institutions.

© 2026 Unlock Your Wealth and Success™. All Rights Reserved.

Terms of Service