How this mortgage affordability calculator works?

Our Mortgage Affordability Calculator helps you estimate how much house you can afford based on your income, existing debt, interest rate, and lender qualification standards. Unlike a basic mortgage payment calculator that only estimates monthly payments, this tool focuses on borrowing capacity using industry-standard debt-to-income (DTI) ratios.

When applying for a home loan, lenders evaluate your financial profile to determine how much risk they are taking by approving your mortgage. The most important metric in this evaluation is your debt-to-income ratio.

This calculator uses the same core framework that many conventional lenders apply during mortgage underwriting to estimate your maximum affordable home price.

Understanding Debt-to-Income (DTI) ratios

Debt-to-income ratio compares your total monthly debt payments to your gross monthly income (before taxes).

Mortgage lenders typically evaluate two types of DTI:

Front-end ratio (housing ratio)

The front-end ratio measures how much of your gross monthly income is spent on housing expenses alone.

Most conventional loan programs follow a guideline of:

28% of gross monthly income

Housing costs include:

Mortgage principal

Mortgage interest

Property taxes

Homeowners insurance

For example, if your annual income is $84,000, your gross monthly income is $7,000.

Using a 28% housing ratio, your maximum monthly housing cost would be approximately $1,960.

This ensures your mortgage payment remains manageable relative to your income.

Back-end ratio (total debt ratio)

The back-end ratio includes all recurring monthly debts in addition to housing expenses.

Most lenders use a guideline of:

36% of gross monthly income

This includes:

Mortgage payment

Car loans

Student loans

Credit card minimum payments

Personal loans

Other installment debt

If your monthly income is $7,000, your total debt obligations should generally not exceed $2,520 under standard guidelines.

This calculator applies both front-end and back-end limits to estimate your safe borrowing range.

Why mortgage affordability matters?

Many buyers focus only on whether they can qualify for a mortgage. However, qualification does not always equal comfort.

A home may be technically affordable under lender standards but still stretch your budget.

Using a mortgage affordability calculator allows you to:

Estimate borrowing power before house hunting

Compare different interest rate scenarios

Adjust down payment amounts

Understand how existing debt affects approval

Plan financially before applying

This helps prevent financial strain after closing.

How interest rates affect home buying power?

Interest rates significantly impact how much house you can afford.

Lower mortgage interest rates:

Increase your maximum loan amount

Reduce your monthly payment

Lower total lifetime interest cost

Higher mortgage interest rates:

Decrease borrowing capacity

Raise total repayment amount

Reduce home affordability

Even a 0.5% increase in mortgage rates can reduce purchasing power by tens of thousands of dollars.

For this reason, comparing interest rate scenarios using this calculator is essential when evaluating housing budgets.

The role of down payment

Your down payment directly increases your purchasing power.

A higher down payment:

Reduces loan principal

Lowers monthly mortgage payment

May eliminate private mortgage insurance (PMI)

Improves loan approval chances

Strengthens your application profile

For example, increasing your down payment from $20,000 to $40,000 could increase the home price you qualify for without raising monthly obligations significantly.

This calculator factors down payment into total affordability to give you a realistic estimate.

Property taxes and insurance considerations

Property taxes and homeowners insurance are often overlooked by first-time buyers.

However, lenders include these costs when calculating mortgage affordability because they are mandatory components of housing expenses.

Property taxes vary by state and municipality, while insurance costs depend on location, property value, and coverage type.

Underestimating these costs can reduce your true borrowing capacity.

This calculator includes tax and insurance estimates so you can simulate real-world affordability more accurately.

What this mortgage calculator does not include?

While this mortgage affordability calculator provides a strong estimate, it does not include:

Private mortgage insurance (PMI)

Homeowners association (HOA) fees

Adjustable-rate mortgage changes

Closing costs

Credit score-based rate adjustments

Lender-specific underwriting overlays

Final mortgage approval depends on a full review of your financial documents, credit profile, employment history, and asset verification.

Always consult with a licensed mortgage professional before making purchase decisions.

Frequently Asked Questions

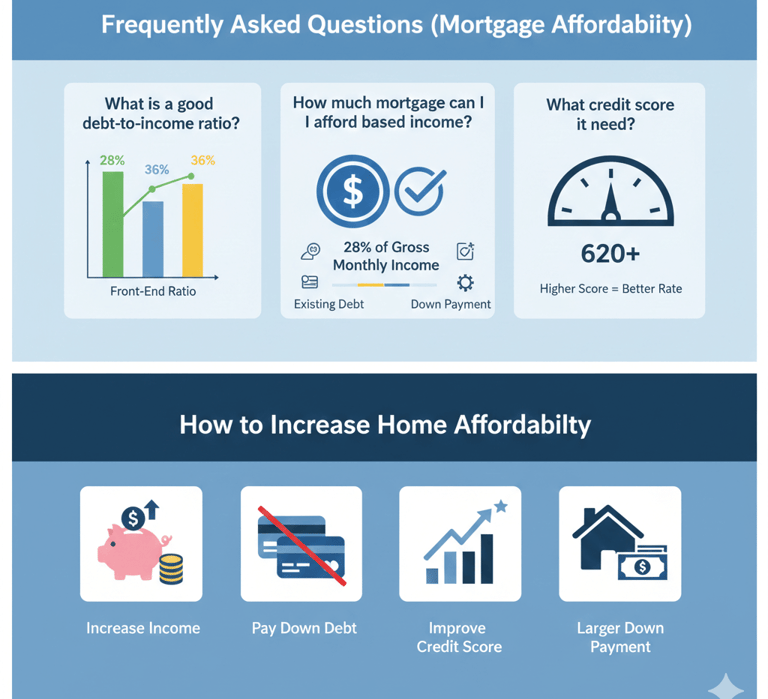

What is a good debt-to-income ratio for a mortgage?

Most conventional lenders prefer:

28% front-end ratio

36% back-end ratio

Some government-backed loans may allow higher DTI ratios depending on credit strength and compensating factors.

How much mortgage can I afford based on income?

A common rule of thumb is that your total housing payment should not exceed 28% of your gross monthly income. However, your exact borrowing power depends on:

Existing debt

Interest rate

Down payment

Property taxes

Insurance costs

Using a mortgage affordability calculator gives a more accurate estimate than general rules of thumb.

Does this guarantee mortgage approval?

No. This tool provides an estimate based on standard lending guidelines. Final approval depends on lender underwriting, documentation, and financial review.

How can I increase my home affordability?

You can increase mortgage affordability by:

Paying down existing debt

Increasing your income

Improving your credit score

Saving for a larger down payment

Shopping for lower mortgage rates

Even small financial improvements can significantly impact borrowing power.

What credit score do I need for a mortgage?

Most conventional loans require a minimum credit score of 620, though higher scores typically qualify for better interest rates and loan terms.

Is it better to put 20% down?

Putting 20% down can eliminate private mortgage insurance and reduce monthly payments. However, many loan programs allow lower down payments if you meet other financial criteria.

Should I buy at the maximum I qualify for?

Not necessarily. Just because you qualify for a certain amount does not mean it fits comfortably within your lifestyle budget. Always consider future expenses and emergency savings.

Final Thoughts

Buying a home is one of the largest financial decisions most people will make. Understanding your mortgage affordability before starting the home search process can prevent costly mistakes and long-term financial stress.

This mortgage affordability calculator helps you estimate borrowing power using industry-standard guidelines so you can plan confidently and responsibly.

Use this tool alongside our other financial calculators to build a complete financial strategy before committing to a mortgage.

Use our Loan Payment Calculator and Retirement Calculator to evaluate monthly payments and long-term financial impact.

Independent financial planning tools for educational purposes only. Not affiliated with Google, AdSense, or financial institutions.

© 2026 Unlock Your Wealth and Success™. All Rights Reserved.

Terms of Service